by Lynda Hughes, Head of Direct Pensions at Davy Select

As life expectancy rises, many of us can expect 45 years in employment followed by 30 years of retirement, possibly living on until we’re in our nineties. So, how can you make sure you’re not left out of pocket for three whole decades? The simple answer: plan effectively.

Don’t forget that generous tax relief is available on qualifying pension contributions. Make sure you avail of the limits available to you at each stage of your working life, seeking tax advice if necessary.

Follow our decade-by decade pointers below to help keep you on track.

In your 20s

– Make sure you open a pension account if you do not have one through your employment

– Save what you can through your pension

In your 30s

– Reassess your debts and outgoings

– Where possible try to increase any contributions you make to a pension account

– Think long-term with your investments

In your 40s

– If you haven’t started saving, do something about it!

– Keep building your pension account

– As your earnings increase – dedicate more to a pension

In your 50s

– Try to maximise your pension contributions

– Reassess your investment risk

– Consider a retirement date and think about the retirement options open to you on retirement– this might not be definitive but set this as a goal

In your 60s

– Check that all your debts, including mortgage, are in order

– Decide when you want to draw down your pension

– Look at the options available to you before you proceed with drawing down your pension

The most important point is to set up a pension account to start saving for your retirement, rather than not do anything at all.

There are a few smart tactics to be considered to keep pension plans on track, depending on the types of pensions an individual may hold and where they are in their life cycle.

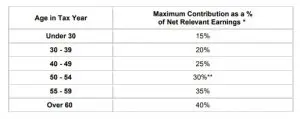

Tip 1: Make the most of the tax relief available to you

If you are a higher rate of tax payer you should contribute as much as you can afford to avail of tax relief at 40% (2022 rate) subject to the maximum contribution limits. Below please find a chart which will provide you with an outline of the maximum allowable limits for personal contributions:

Tip 2: Use the October 31st deadline

Individuals are entitled to make either a Personal Pension Plan (RAC: Retirement Annuity Contract), PRSA (Personal Retirement Savings Account) or AVC (Additional Voluntary Contributions) payment before October 31st and backdate this against their 2021 earnings.

For those who pay and file their return online under Revenue’s On-line Service (ROS) the deadline is extended to 16th November 2022. This could potentially reduce your tax liability for 2021. (See table 1 above for a breakdown of the maximum allow limits).

Tip 3: Consider your risk profile as you get closer to retirement

When you are younger you can afford to adopt a higher level of risk as you are investing for the longer term. As you get older you should consider reviewing your level of risk, taking into consideration the value of your overall pension pot and income requirements in retirement.

Tip 4: Tidy up your existing pension arrangements

Many individuals change employment on a number of occasions during their working lifetime. As a result they may have more than one pension account. It may be worthwhile reviewing other pension arrangements to make it easier for you to keep an eye on the value of your total retirement savings, in addition to having an investment strategy that you are happy with.

Tip 5: Be aware of your fees and charges

Charges can have a big impact on the overall pension fund value that you have upon reaching retirement. You should consider reviewing these fees and charges to ensure that you are receiving a competitive charging structure that is consistent across the marketplace.

About the author

Lynda Hughes is head of Direct Pensions in Davy Select. Lynda joined Davy in 2006 and initially worked in Financial Planning before taking up her role in Davy Select in 2012. Prior to joining Davy, she worked with as a Financial Planning Consultant with AIB. Lynda Is CFP qualified. In addition, she holds an MSc in Financial Services from UCD.

If you would like to discuss the pension options available to you, please contact the Davy Select Pension Team, email pensions@davyselect.ie or click here for more information on Davy Select pensions.

{kind=link}