by Jillian O’Sullivan, Partner, Corporate Compliance at Grant Thornton

The Irish Minister for Finance, Pascal Donohue, presented his budget for 2026 to the Irish Parliament on Tuesday, 7 October. See the full analysis of the main changes impacting your company and payroll from 1 January 2026.

Main changes impacting your payroll

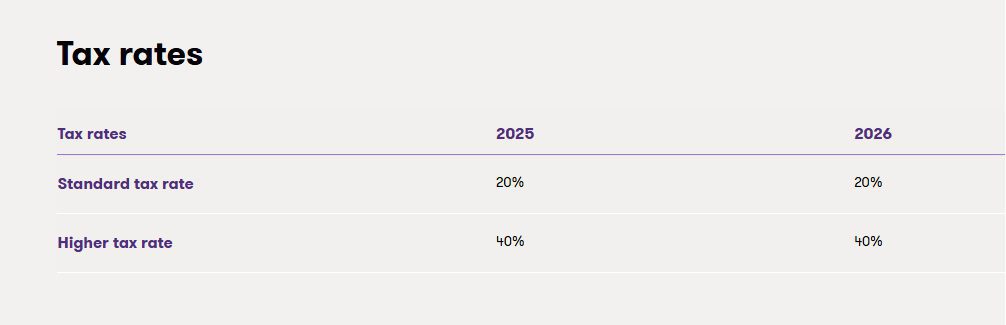

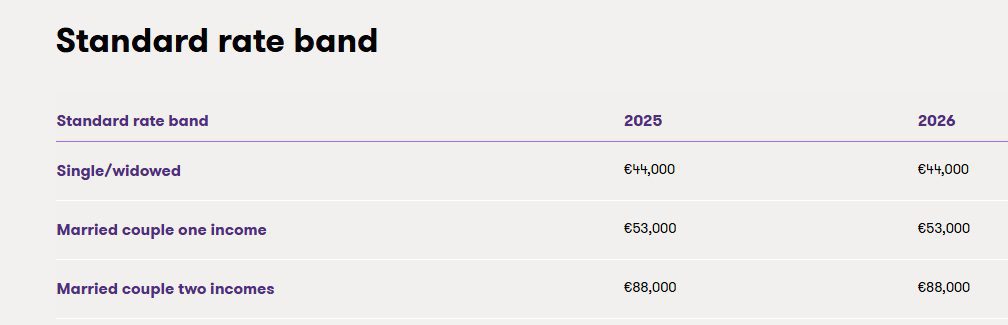

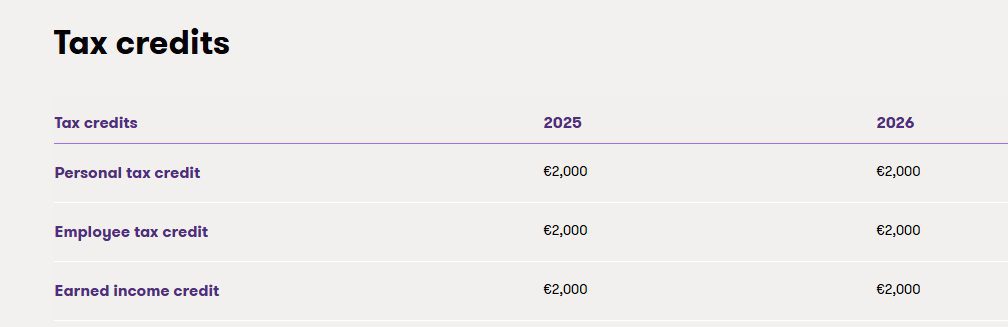

Standard rate tax bands

No increase in standard rate band or tax credits in 2026.

Foreign earnings deduction (FED)

- FED extended to 2030, and the maximum relief increases from €35,000 to €50,000 from 1 January 2026.

- The Philippines and Turkey are now included in the list of relevant States.

Universal Social Charge (USC)

- The 2% USC band will increase by €1,318 to €28,700.

- Reduced USC rate will continue to apply (to 31 Dec 27), when an individual holds a full medical card and earns up to €60,000.

BIK company car

- The temporary OMV €10,000 reduction extended to 2026 and tapered thereafter to €5,000 in 2027 and €2,500 in 2028.

- A new A1 category to be introduced for vehicles with zero emissions, the reduced BIK rates will range from 6-15% depending on business mileage.

Rent tax credit

Extended for a further 3 years to 31 December 2028 (up to €1,000 per person per annum).

Minimum wage

Minimum wage to increase by 65c to €14.15 per hour with effect from 1 January 2026.

Key Employee Engagement Programme (KEEP)

KEEP extended to 31 December 2028, subject to approval by the European Commission.

PRSI rates

A further increase in PRSI contribution rates of 0.15% for both employers and employees from 1 October 2026, as previously announced.

Special Assignee Relief Programme (SARP)

- SARP extended to 2030, with the minimum salary requirement increased from €100,000 to €125,000 from 1 January 2026.

- Administrative requirements to be simplified – further detail expected in Finance Bill.

Further updates

Provision of staff meals

Revenue released new guidance that outlines the tax treatment of meals provided to employees. Effective from 1 October 2025, no taxable benefit in kind will arise in respect of meals provided to staff provided in specific scenarios as follows:

- Meals provided to all employees on the employer’s premises and consumed on site;

- Working lunches/dinners provided to certain employees on the employer’s premises where there is a business requirement and the cost per employee does not exceed the civil service subsistence day rate, which is currently €19.25.

Karshan disclosure opportunity

Revenue recently announced that employers can enter in to a PAYE settlement arrangement where certain individuals were incorrectly classified as self-employed rather than employees for the tax years 2024 and 2025. The submission deadline is 30 January 2026.

This follows the Supreme Court’s 2023 judgment in Revenue Commissioners v Karshan (Midlands) Ltd, which clarified how to determine whether a worker is an employee or self-employed for tax purposes. This arrangement provides an opportunity for employers to correct their PAYE position for 2024 and 2025.

Auto Enrolment (AE) retirement savings scheme

The Auto Enrolment (AE) retirement saving scheme, referred to as “My Future Fund,” to be established for employees who do not currently participate in a pension scheme.

The AE mandatory obligation for employers is set to launch on 1 January 2026. As outlined in Budget 2026, additional amendments addressing participant death, tax exemption for AE provider schemes from investment undertaking tax, and an exemption from the Universal Social Charge (USC) for employer contributions to AE, to be addressed in Finance Bill 2025.

Small benefit exemption

No changes to small benefit exemption up to five non cash benefits can be provided tax free to a total value of €1,500 in a tax year.

About the author

Jillian O’Sullivan leads the company secretarial and employer solutions team at Grant Thornton, which includes the provision of outsourced payroll services. She assists companies establishing a presence in Ireland, from their initial setup to their on-going compliance, payroll and other outsourced service requirements. She also deals with all areas of corporate compliance and governance. Jillian has significant experience in the restructuring of corporate entities and groups, both medium and large, and in the implementation of related tax planning and succession schemes. She lectures extensively and facilitates seminars on both the role and responsibilities of directors in companies.

{kind=link}